If you are someone who recycles, buys fair trade, and has a 401k, it’s time to think about going ESG with your portfolio. Here’s why it’s worth going ESG, what it even is, what it’s not, what the best options are, and how to easily do it while being financially smart.

Many of us rightly criticize companies like WalMart, Exxon, Monsanto, McDonalds, and Lockheed Martin for their immoral business practices; however, everyone with a typical 401k owns stock from them. If the idea that your retirement is being paid for by causing climate change, corrupting governments and exploiting workers makes your blood boil, then you’ll be happy to know, it’s now (finally!) possible to divest from these companies and still have a financially smart retirement portfolio.

While socially responsible investment (SRI) funds have existed for decades, they’ve generally been expensive, actively managed funds only available to institutional investors. It’s only in the past 5 or so years that a wide variety of environmental, social and corporate-governance (ESG) index funds have become generally available for retail investors in the United States.

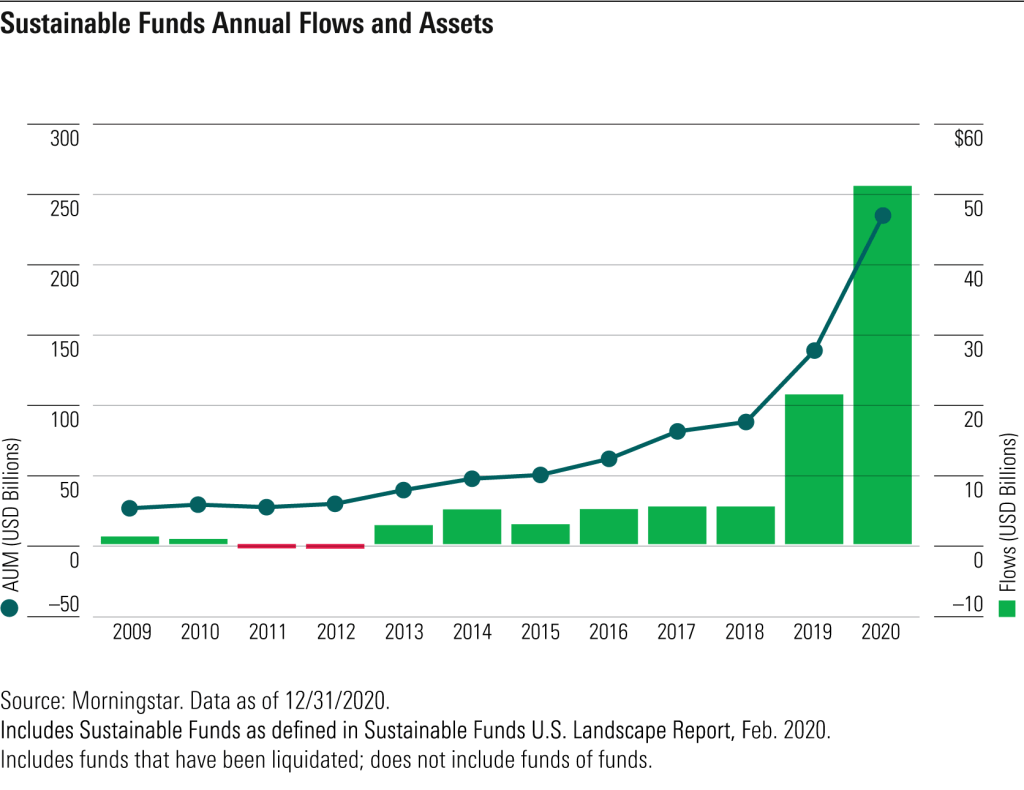

Europe is still way ahead of the US here. According to Morningstar, 77% of sustainable funds and 81% of assets held in sustainable funds are based in Europe. The US has a measly ~400 ESG funds compared to Europe’s ~3200 (half of which have been launched in the past 4 years). But American socially responsible investing has started taking off: US ESG capital inflows in 2020 were $50T, 10x what they were in 2018.

Even more exciting, while 62% of sustainable funds in the US are still invested in actively managed funds, in 2020, passive index funds attracted 70% of all sustainable capital inflows – driven largely by iShares launching a whole suite of ESG index funds in October 2020 that are both more rigorous and cheaper than other ESG index funds available on the market.

This was very exciting for me because it meant that I could realistically invest most of my portfolio in ESG funds (with the exception of government bonds and gold – for which ESG as a criteria is a bit meaningless). But all the ESG research I’ve done was unnecessarily time consuming and tedious, so I figured I’d make it easier for others and share what I’ve learned.

What ESG is and what it is not

The first thing to understand about ESG investing is that the industry approaches and defines ESG in terms of business risk rather than morality. In other words, systems like Morningstar and MSCI are not quantifying morality, but instead are quantifying the Environmental, Social and Governance business risks and opportunities that come as a consequence of moral or immoral behavior. This makes ESG investing a proxy for moral investing, but it’s important to understand that morality and business risk due moral behavior are not the same.

Note: this is a great example of the toxicity of capitalist logic where the value of moral behavior must be justified in terms of business risk/return, rather than morality just being a valuable end unto itself.

The next thing to know is that what constitutes E, S, or G risk is highly subjective and difficult to quantify, and most interpretations of the bar needed for a fund to qualify as ESG are milquetoast. The vast majority of ESG index fund’s top 20 holdings include companies like Amazon, Facebook, and Bank of America and will still invest in industries like fossil fuels, military weapons, predatory lending, private prisons and more. Even my favorite, relatively ESG-rigorous index funds still include companies like Verizon, Pepsi, and Morgan Stanley (check links for more info on dubious behaviors).

It’s plenty obvious that a company like Shell faces environmental risk due to things like climate-related regulations, social risk for exploiting laborers in Nigeria, and governance risk for coercing workers to attend a Trump rally – and this will be consistently captured by any ESG rating system. But how much environmental risk does Hasbro face now that it is phasing out plastic in its packaging but not its toys?

So while you’ll have broad alignment between systems from Morningstar or MSCI on what is more or less ESG, you can also get some major discrepancies. For example, Invesco’s PICB fund is rated by MSCI as the top 9th ESG percentile among all funds, while Morningstar placed it in the 54th percentile for Sustainability.

Part of what’s going on here is that the ESG space is still nascent and has a long way to go, but part of it is the impossibly difficult nature of the problem the financial industry is trying to solve. Quantifying the environmental, social and governance practices of a corporation and then creating formula for how you include and weight them in an index that is still diversified and reflects the underlying market capitalization as best it can given your moral criteria – that’s really hard, understandably takes time and money, and ultimately has no correct answer.

This problem requires a tremendous amount of research, ideological refinement, and mathematical know-how – and that only comes with time and investment – a process we can accelerate by putting our money in less-than-perfect ESG funds today.

Why it’s worth investing in ESGs

1. Market pressure – When capital increasingly flows into ESG funds, bloodthirsty capitalists take notice. They will smell profit and respond in a pro-ESG fashion – even if it is for cynical motives. This is what happened with organic, all-natural, fair-trade and animal welfare products. The people who spent decades “over-paying” at WholeFoods are the reason that Walmart, Stop & Shop and virtually every grocery store now carries more morally produced products. Just look at the explosion in number of fair trade certified products over the past couple decades (in millions):

The same thing is already happening with ESG investing. Even Shell Oil now has an entire web-page dedicated to explaining it’s ESG actions and principles, and ESG is now the topic-du-jour for the mining industry. This should all be viewed with skepticism, but the point is ESG investing is already having such an impact that fossil fuel and mining companies feel compelled to respond to it.

Those that pay a premium for a sub-optimal ESG product today will accelerate the maturation of ESG thinking in the broader investment world. Buying ESGs is not just about the impact you will have today, it is also a down-payment toward building a better world for others in decades to come.

2. Investor activism – Investment firms that hold our money vote on our behalf at shareholder meetings. Most of them (BlackRock, Vanguard, Fidelity, Deutsche Bank etc.) have atrocious ESG proxy-voting records. These firms may be tip-toeing towards better ESG practices, but what real changes they make remains to be seen. For their services, you will be charged .10% to .35% expense ratios. If you are willing to go up in price to .20% to .40%, you can invest in similar index funds at a firm like Nuveen and get a strong track record of proxy voting. Per $100,000, that comes to $100-$300 more per year – call it charity.

If you want more ESG-ethics, you have to shift to actively managed funds. For .75% to 1.5%, you can invest with firms Calvert, Parnassus or Impax. They largely offer actively managed funds where they are not just thoughtful about what companies they invest in and how they vote at shareholder meetings, but they will also engage with executives and even sometimes drive shareholder activism.

Ultimately, you pay for what you get. Prices on ESG funds are still high, but coming down and will continue to with growing economies of scale.

Side-note: if your 401k is in a standard retirement fund, there’s a good chance you are being ripped off. My 401k’s Target Retirement funds from Putnam carry a .50% expense ratio – higher than any ESG funds I’m invested in.

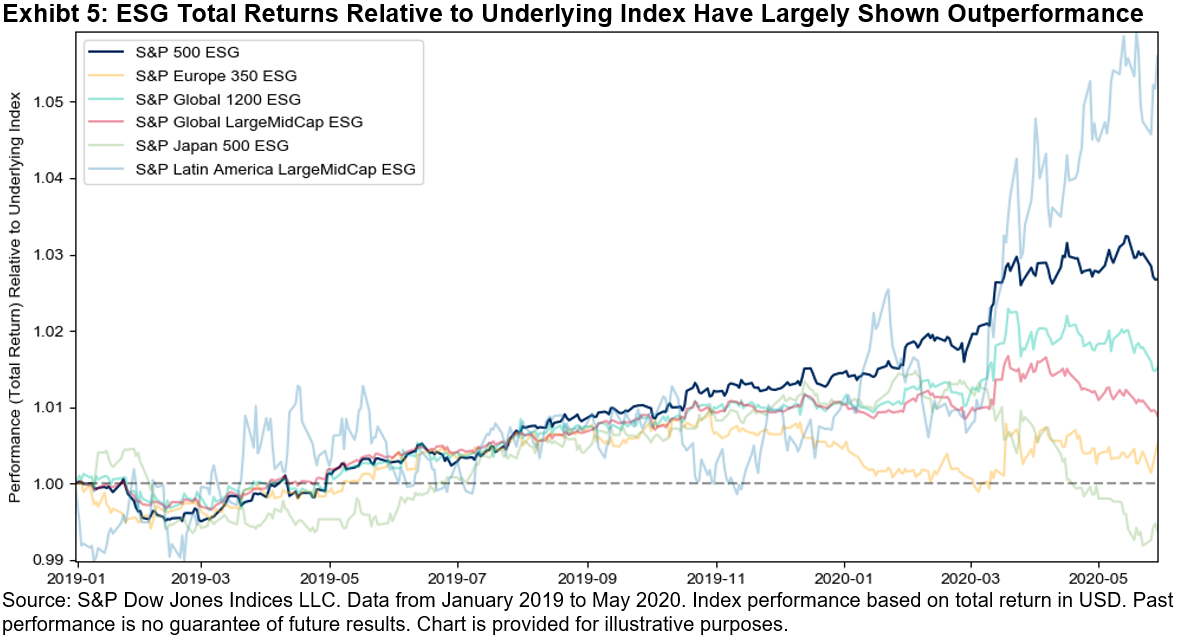

3. Personal returns – While ESG index funds come with expense ratios 2x-4x those of the cheapest available index funds (usually Vanguard), going ESG may actually still be more profitable. This is because, so the theory goes, that those companies most ESG oriented have reduced business risk and thus better set themselves up for long-term competitiveness and profitability – and this appears to be validated by the data.

Over the past 30 years, the KLD Social 400 (one of the oldest socially responsible indexes) beat the S&P 500, and over the past 10 years, 80% of large-cap ESG index funds have outperformed their non-ESG counterparts. As a result, 85% of all funds now incorporate ESG factors in their analysis.

the groundbreaking insight: morality is profitable

galaxy brain Wall Street

4. Purifying one’s soul – this is, in my opinion, the least important factor simply because every time we go to the gas station or buy bottled water… we taint our souls. Consumer and investor activism has its limits and can’t solve problems that require political solutions. But nonetheless, even the ocean is made up of water droplets. You can either be part of the problem or feel better knowing your retirement is being financed by a lot less harm.

Besides: there’s nothing like sipping Chardonnay and caviar at a party on the Upper East Side while shaming liberals for not being as woke as you are (don’t bother trying this with Republicans… they tend to have no shame and will just smirk at you for being so naive and idealistic as to care about the world).

ESG index fund options

While the majority of ESG funds are actively managed, on average passive funds generate higher returns – so I am going to limit my discussion to index funds. When talking about passive ESG investing, it’s important to first acknowledge that even if you are investing in ESG index funds, they are more expensive and less diversified than normal index funds. Usually, less diversification means more risk, but ESGs are an explicit de-risking strategy, so it’s hard to say what the net effect is on one’s portfolio. It also depends on what ESG methodology one uses: ESG index funds can range from covering 94% of their parent index, to 50%, to as little as 25%.

ESG methodologies can be understood in terms of three strategies: positive, negative and impact. Virtually all ESG index funds do some level of negative screening, and some will also do positive or impact weighting on top of that.

- Negative screens exclude industries to varying degrees that are deemed not-ESG friendly.

- Positive screens invest in companies with the higher ESG ratings in each sector.

- Impact screens only invest in companies that explicitly contribute to solving a dimension of the E, S, or G factors.

Of the five leading ESG index providers, MSCI has the most comprehensive and representative system – with 7-15 types of methodologies depending on how you count.

- Universal is the most basic negative ESG screen that MSCI has. This just screens out companies that are involved in controversial weapons and violate UNGC principles (such as profiting from land mines, or biological and chemical weapons) and does nothing else.

- ESG Screened adds nuclear weapons, tobacco, thermal coal, oil sands and civilian firearms to this negative screen list. Focus has these same screens but then also positively weights the index towards high-ESG companies.

- Leaders and Select add conventional weapons, alcohol, nuclear power and gambling to their negative screens list. Leaders then positively screens for just the top 50% of ESG companies in each sector, while Select seeks to just reflect the underlying index.

- The Faith Based, SRI and KLD methodologies, add GMOs and adult entertainment to the negative screen list. Faith based is just a negative screen, while SRI then also limits itself to just the top 25% of ESG companies in each sector, and KLD just seeks to invest in companies that are limiting their ESG risk.

- The Choice Screened negatively screens all of the above and adds predatory lending, private prisons and palm oil to the list.

- Beyond these, MSCI offers a host of positive environmental indexes (Climate Paris Aligned, Climate Change, and Low Carbon), as well as, impact indexes (Global Environmental, Sustainable Impact and Women Leadership). All of these do a mix of negative screens and positive weighting or impact selection.

You’ll note though, while this sounds like a lot, it actually doesn’t give us many options. What if you are like me and want to divest from private prisons and predatory lending, but think that nuclear power is environmentally friendly, wish that more nuance were applied to a category like GMOs, and don’t care about divesting from things like alcohol or adult entertainment? You don’t get much choice. It’s an all or nothing proposition.

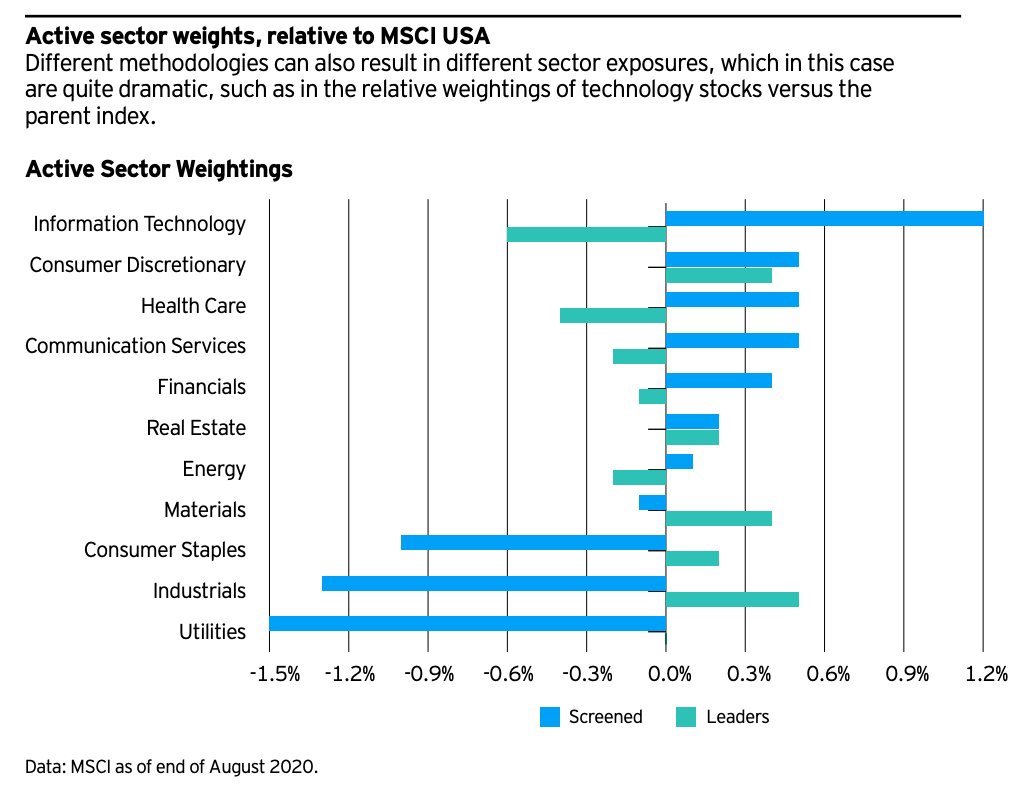

And as one looks further under the hood, which methodologies are more or less ESG also becomes more difficult to interpret. For example, which of the following funds (USXF and SUSL) is better from an ESG perspective?

MSCI rates the former slightly higher (97th peer ESG percentile) than the latter (95th percentile) – but when I look at these charts, the carbon intensity, green vs brown revenue, board diversity and board independence statistics from MSCI, it looks to me like the latter is slightly better from an ESG perspective.

My conclusion after all of this is that it’s a bit of a crapshoot knowing exactly what the most moral or financially sound ESG methodologies are – but there are clearly better and worse ESG funds, indexes and investment firms to choose from.

How to go ESG

Going ESG is a matter of degrees. Truly going ESG and still maintaining a well-diversified and low-cost portfolio necessitates investing in multiple funds – at minimum 3 or 4, but more realistically 10-20 total. And to manage this, you’ll have to build a whole spreadsheet system that enables you to calculate your target allocation, current asset allocation and how to rebalance your portfolio (see resources at end for more information on how to do this).

If you want just one single ESG fund with a Target Retirement date that does all this work for you, your only options are the Natixis funds (pretty good ESG-wise, but really expensive and small – which risks fund closure) or BlackRock’s LifePath funds (barely qualifies as ESG but very reasonably priced). Depending on where your money is sitting, you may not even be able to invest in either of these funds anyway.

If you are willing to put a bit more effort into your ESG investing and want to keep your expenses as low as possible while maintaining a decent level of ESG rigor, you can build your entire portfolio out of iShares’ 28 ESG funds. The downside of iShares is that its parent company, Black Rock, has a dubious ESG track record (receiving a ‘Basic’ ESG Commitment level rating from Morningstar) and has only recently gotten serious about reversing this.

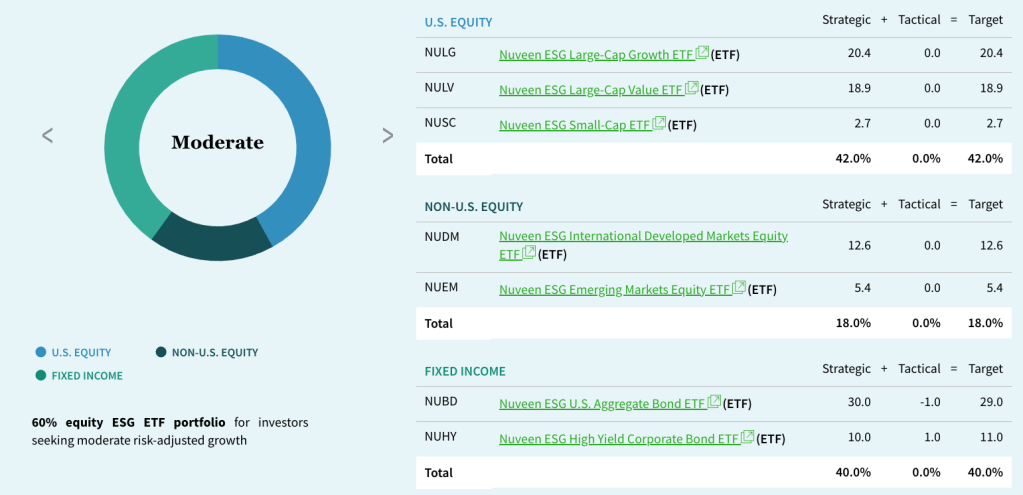

If you want to be maximally pro-ESG while still being in index funds and are willing to pay a price for it, I recommend Nuveen’s funds. They were rated ‘Advanced’ by Morningstar due to their ESG index design, as well as, their long track record of pro-ESG proxy voting. You can use Nuveen’s tool to easily figure out how to build a well-balanced portfolio.

But really doing ESG right requires analyzing and comparing the available funds, their investment methodologies and firms in each asset class separately. These come with different tradeoffs around expense ratios, volatility, tracking errors and industry exposure/weightings – all of which are not necessarily related to the degree of their ESG rigor and vary based on which asset class the ESG methodology is being applied to.

Among equities, international developed stocks have the highest ESG ratings (mainly due to European and Japanese regulation being the most ESG friendly already), followed by US stocks (large cap, then mid-cap, then small-cap), with emerging markets and REITs being the least ESG-friendly categories of all.

Bond funds typically have very high ESG ratings. But this is deceptive, because the majority of them are invested in government bonds and mortgage backed securities – both of which are meaningless from an ESG perspective.

My ESG investment strategy

My investment strategy basically boils down to having multiple ESG index funds within each asset class (when possible) so as to diversify between MSCI ESG methodologies and their moral, cost, and risk tradeoffs.

ESG Equities: When it comes to US, International Developed Markets and Emerging Markets Equities, my strategy is to primarily have a mix of ESG Leaders and Choice-Screened funds – mostly from Nuveen (TIAA) and iShares (BlackRock) – with a couple Sustainability Impact and Focus funds. While I would’ve liked to include more ESG funds from other firms (notably at the cheap end from DWS, Vanguard and Fidelity), ultimately, I feel that Nuveen and iShares offer the best ESG-methodologies and practices with the best expense ratios at their respective price tiers.

I’m most partial to Nuveen’s index funds because of their proxy voting record, mid-level expense ratios and Low-Carbon Leaders methodology. This comes at a cost though, so I balance this with some iShares Leaders funds that have very low expense ratios. Not wanting to be overexposed to just the Leaders methodology, I’ve also incorporated Choice-Screened funds from iShares. These boast both the lowest expense ratios of all ESG funds on the market and notably screen out private prisons and predatory lending.

The additional benefit of mixing Choice-Screened with Leaders is that the two indexes have very different industry exposures in opposite directions relative to the parent index. So by using both, it cancels out some industry diversification risk.

ESG Bonds: When it comes to ESG bond funds, there’s limited selection. These ESG bond funds carry a higher expense ratio that really hurts for an asset class that generates relatively low returns to begin with (especially now in a 0% interest era) – and where it’s difficult to justify paying more to invest in government bonds and mortgage backed securities where no ESG screens are applied anyway. As a result, I just buy regular index funds for government bonds, and then do ESG corporate bond funds using the Focus, Choice-Screened, and Select methodologies with the lowest expense ratios in their bond sub-classes.

Note: so many investment firms are changing their ESG practices and launching new funds with new methodologies and lower expense ratios that this entire analysis and strategy could well be dated within 1-2 years. I certainly hope so.

The top 20 ESG ETF index funds I considered for my portfolio

| Asset Class | Ticker | Firm | Exp. Ratio | MSCI Methodology | ESG Peer Percentile |

|---|---|---|---|---|---|

| US Large Cap | USXF | iShares | .10% | Choice-Screened | 97 |

| US Large Cap | NULC | Nuveen | .20% | Low-Carbon Leaders | 98 |

| US Large Cap | SUSL | iShares | .10% | Extended Leaders | 95 |

| US Mid Cap | NUMV | Nuveen | .40% | Low-Carbon Leaders | 100 |

| US Mid Cap | NUMG | Nuveen | .40% | Low-Carbon Leaders | 100 |

| US Small Cap | ESML | iShares | .17% | Extended Focus | 86 |

| US Small Cap | NUSC | Nuveen | .40% | Low-Carbon Leaders | 99 |

| Global Stocks | SDG | iShares | .49% | Sustainability Impact | n/a |

| International Developed | DMXF | iShares | .12% | Choice-Screened | 95 |

| International Developed | NUDM | Nuveen | .40% | Low-Carbon Leaders | 96 |

| Emerging Markets | LDEM | iShares | .16% | Extended Leaders | 78 |

| Emerging Markets | EMXF | iShares | .16% | Choice-Screened | 95 |

| Emerging Markets | NUEM | Nuveen | .45% | Low-Carbon Leaders | 81 |

| US Aggregate Bond | EAGG | iShares | .10% | Extended Focus | 98 |

| US Aggregate Bond | NUBD | Nuveen | .20% | Select | 97 |

| Global Bond | BGRN | iShares | .20% | Green Select | 92 |

| Global Corp. Bonds | SUSC | iShares | .18% | Focus | 99 |

| Global Corp. Bonds | SUSB | iShares | .12% | Focus | 100 |

| High Yield Corp. Bonds | HYXF | iShares | .35% | Choice Screened | 98 |

| High Yield Corp. Bonds | NUHY | Nuveen | .35% | Select | 98 |

For your convenience, I’ve compiled my preferred ESG index funds into this Google Sheet. Just make a copy and play around with it as you see fit.

Further information and tools to help go ESG

To better understand ESGs, read:

- ESG Firm and Fund Commitment – Morningstar

- A Guide to Comparing ESG ETFs – Invesco

- MSCI Indexes Explained – MSCI

- Extended Focus and Choice-Screened Indexes Explained – MSCI

To research ESG funds, use:

- ESG Fund Rating Tool – MSCI

- ESG Fund Screener – Morningstar

- ETF Screener – ETF Database

To get a basic introduction to investing, start with this Concise Guide to Asset Allocation from Lyn Alden. I highly recommend checking out her website as she has posts explaining all sorts of topics for every level of investing sophistication. Beyond that, the following are some good primers:

- Everything You Need to Know About Bonds – PIMCO

- REIT vs Bond Funds – Simple Smart Income

- US vs International Stock Allocation – Wall Street Physician

- International Equity Allocation – WMS Partners

- How to Choose the Right Bond Funds – The Balance

- Global Equity Investing – Vanguard

- Equities Post-Covid – Touchstone Investments

- REIT Asset Allocation – Seeking Alpha

Closing thoughts

Though there are diminishing marginal returns to time spent learning about investing, it is critical that every individual builds up a baseline of knowledge. Many people lose a lot of hard-earned-money and endanger their retirements by making basic investing mistakes like buying individual stocks (like GameStop), setting overly-risky asset allocations (ie not matching one’s glide path or not having a safety net for 1-3 years), or then selling stocks while the stock market crashes (you should be doing the opposite, rebalancing your portfolio selling bonds to buy stocks).

Setting one’s asset allocation and picking one’s funds is the major ACTIVE decision anyone makes in their entire investment process – even if one ultimately goes with index funds. At this juncture, it is critical one has learned enough to be adequately informed given one’s level of capital. But no matter how much research one does and how nuanced one gets, the decision will ultimately have a significant element of randomness and luck.

Going with passive index funds introduces diversification and reduces personal bias risk, randomness risk, and costs of management and transactions – which increases returns on aggregate in the long run. By going with ESG index funds we increase our expenses and decrease our diversification – which would normally mean increased risk, but by going ESG we’re also intentionally de-risking our portfolio. What impact that has on returns only the Invisible Hand knows; however, what we can know is that our decisions as individual in the marketplace do affect market prices and trends in a microcosmic fashion.

When you put your finger on the market in a moral manner, those ripple effects will have moral outcomes – and that is why, no matter what crapshoot you decide to take with your 401k, you should at least make it a moral one and go with ESGs.

Thanks for reading!

Many thanks to my father, Heri, for helping with all this research and teaching me so much.

If you enjoyed this and want to join my mailing list, please subscribe. I might write about politics, philosophy, education, business or technology.